Returns Are Gaining Momentum At EROAD (NZSE:ERD)

You may not have known that there are financial metrics that can give clues to a potential multibagger. We’ll first need to see the proven Return Capital employed (ROCE) is an increasing number and, secondly, it’s expanding. Base Capital employed. This is a sign that the company has a strong business model and lots of lucrative reinvestment opportunities. We have noticed promising trends at EROAD (NZSE:ERDLet’s dig a little deeper.

Understanding Return On Capital Employed (ROCE)

ROCE measures the’return (pre-tax profit) that a company earns from capital it has invested in its business. To calculate EROAD, analysts use this formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

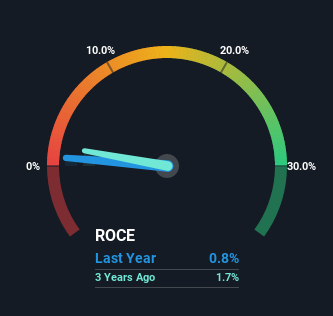

0.0076 = NZ$2.4m ÷ (NZ$390m – NZ$76m) Based on the trailing twelve month period ending in September 2022.

So, EROAD has a ROCE of 0.8%. It is a poor return, and underperforms the Electronic Industry average of 17%.

View our latest analysis for EROAD

The chart above compares EROAD’s ROCE prior to its performance. However, the future is more important. You can view the forecasts of the analysts who cover EROAD if you wish. here For free.

What Does the ROCE Trend for EROAD Tell Us About It?

EROAD is seeing the fruits of its investments, and EROAD is now making some pre-tax profit. This is something we are thrilled about. The business, which was losing money five year ago, is now making 0.8% profit on its capital. Shareholders will be delighted with this. EROAD has 611% more capital now than it did five years ago. This is unsurprising, as most companies are trying to break into the black. We love this trend because it shows that EROAD has profitable reinvestment options available to it. If it continues moving forward, it can lead to multi-bagger performances.

EROAD’s current liabilities have decreased to 19% of total assets during this period. This effectively reduces the availability of financing from short-term creditors or suppliers. So we can be confident that ROCE has grown due to the fundamental business improvements and not a cooking class based on this company’s books.

Our View on EROAD’s ROCE

The bottom line is that we are pleased to see EROAD’s successful reinvestment programs have paid off. The company is now profitable. The stock has fallen 76% over the past five years, so it is possible that other areas of EROAD could be hurting its prospects. It’s worthwhile to do more research to determine if these trends will continue in the future.

Last note: 5 warning signs for EROAD (2 are concerning) You should be aware.

For those who are interested in investing solid companies, This is a great article. Free list of companies with solid balance sheets and high returns on equity.

Give feedback about this article Are you concerned about the content? Get in touch Contact us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article is by Simply Wall St. It is general in nature. We only provide commentary on historical data and analyst projections. Our articles are not meant to be considered financial advice. This analysis does not represent a recommendation to purchase or sell any stock and it does not consider your financial goals or financial situation. Our goal is to provide you with long-term, focused analysis based on fundamental data. Please note that our analysis might not include the latest announcements from price-sensitive companies or qualitative material. Simply Wall St holds no position in any of the stocks mentioned.

Participate in a Paid User Research Session

You’ll receive a Amazon Gift Card – US$30 Give us 1 hour of your time and help us create better investing tools for individual investors like you. Sign up here