Here’s What Analysts are Forecasting Now

You may be familiar with the following: CarMax, Inc. (NYSE:KMXLast week, ) released its third quarter results. Unfortunately for shareholders, it did not go as planned. The overall result was not great. While revenue fell just slightly short of analyst estimates at US$6.5b and statutory earnings missed forecasts by 63%, coming in at US$0.24 each share. This is a critical time for investors as they can track the company’s performance and look at forecasts for next year. Investors can also see if any changes have occurred in their expectations. We thought it would be interesting for readers to see the latest post-earnings forecasts from analysts for next year.

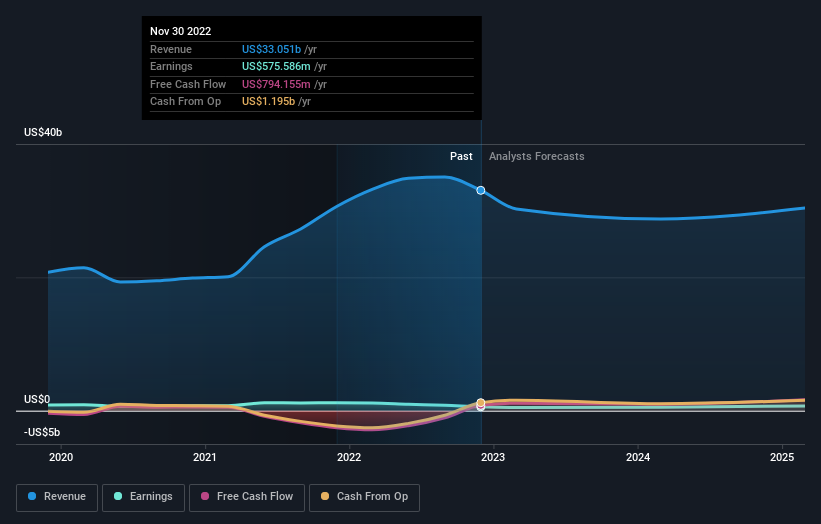

View our latest analysis for CarMax

According to 16 analysts covering CarMax, the consensus is for CarMax revenues of US$28.7b 2024. This represents a substantial 13% drop in sales relative to the previous 12 months. In the same time period, statutory earnings per share will decrease by 8.5% to US$3.33. Analysts had projected revenues of US$31.5b, and earnings per share (EPS), of US$4.39 for 2024 in the period leading up to this report. We can see that sentiment is becoming more bearish since the release of the results. This has led to lower revenue forecasts, and a very serious decrease in earnings per share estimates.

It will not surprise you to hear that analysts have lowered their price target to US$68.20 by 15%. It can be dangerous to fixate on one price target, as the consensus target is the average of all analyst price targets. Some investors prefer to examine the range of estimates to see whether there are diverging opinions about the company’s valuation. The current valuation of CarMax is US$141 per share by the most bullish analyst, while it is valued at US$26.00 by the bearishest analyst. In this scenario, we would assign less value the analyst forecasts because there is a large range of estimates that could indicate that it is difficult to accurately value the future of the business. It might be unwise to base decisions on the consensus price target. This is a composite of a wide range of estimates.

These forecasts can also be viewed in context. industry itself. It is expected that sales will decline, with an 11% annualised revenue drop by 2024. This is a marked change from the 15% historical growth over the past five years. However, our data indicates that revenues for other companies in the industry with analyst coverage are expected to increase by 5.7% annually. It’s clear that CarMax will see its revenues perform much worse than the overall industry.

The Bottom Line

It is important to note that analysts have downgraded earnings per share estimates. This shows that sentiment has declined following these results. They also reduced their revenue estimates. This means that revenues are expected to be lower than the rest of the industry. The analysts also reduced their price targets, which suggests that they are more pessimistic about the business’ intrinsic value.

This being said, the long-term growth of the company’s earnings will be more important than next fiscal year. We have estimates from multiple CarMax analysts going out to 2025. see them free on our platform here.

Also, it is worth noting that our team has also discovered 2 warning signs for CarMax (1 is concerning!) You need to be aware of these things.

Give feedback about this article Have a question about the content? Get in touch Get in touch with us. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St has a general nature. Our commentary is based on historical data, analyst forecasts and other unbiased information. We do not intend to provide financial advice. It is not a recommendation not to buy or sell any stocks and it doesn’t take into account your financial situation or objectives. Our goal is to provide you with long-term, focused analysis based on fundamental data. Our analysis may not take into account the most recent price-sensitive company announcements and qualitative material. Simply Wall St holds no position in any of the stocks mentioned.

Register for a paid user research session

You’ll receive a Amazon Gift Card – US$30 Spend an hour helping us to create better tools for individual investors. Sign up here