Do not get too excited about Nike’s earnings beat

Nike’s fiscal second quarter 2023 financial report was released last week. It revealed some very encouraging results. The company’s revenue grew 17.3% year-over-year, surpassing analysts’ average goal of $740 million. The company also experienced lower input cost pressure which translated into 21 cents per shares earnings above estimates.

The company’s organic growth continues to be evident by a deeper dive in its second-quarter earnings report. Nike Direct sales increased by 25% year-over-year, while wholesale sales rose by 30% and digital sales increased by 34% in the same period.

Increasing digitalization is a major factor in Nike’s organic growth. Because customers can shop online, they can also view, pay and choose their delivery method based on their preferences. Nike’s improved inventory management and consumer targeting are a result better data analytics. This could help the company grow its income in the future.

Despite Nike’s excellent second quarter financial results I still have concerns about the company and its medium-term prospects. Here are the reasons.

Accruals and the risk of a Recession

Nike has exceeded its earnings targets in consecutive quarters but has not delivered adequate earnings per share results in four of the last twelve quarters. This suggests that the stock could be vulnerable to a crash in a recession.

Stock price momentum can be measured either cross-sectionally and/or by time series regression. The latter measures a stock’s price momentum in isolation. It is often caused or influenced by an organization’s earnings momentum. Nike’s earnings crash danger is likely a characteristic of its cyclicality. It could impact the stock’s long-term trajectory.

The company’s exposure to emerging markets could also be a liability, as emerging markets are more at risk of falling into recession. Nike is also heavily discounted by the strong U.S. currency in emerging markets.

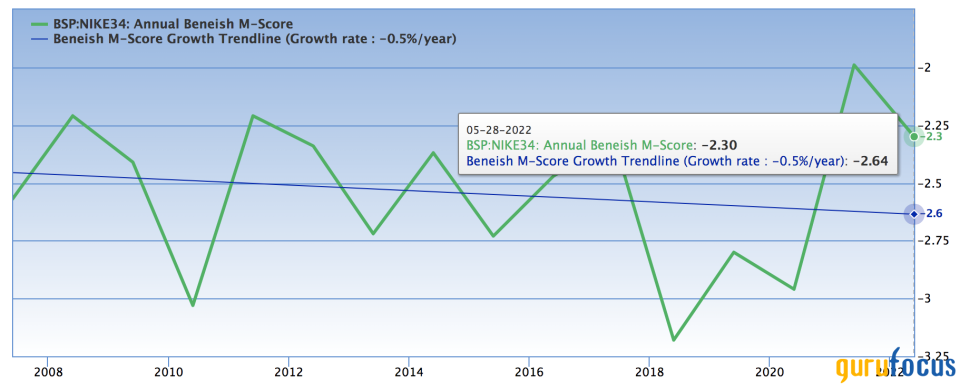

Nike’s Beneish M-Score Investors are happy to hear that a minus of -2.3 is a good sign. The Beneish M score metric measures how aggressive a company’s accounting metrics are. An M-Score below 1.78 indicates that a company’s accounting practice is conservative. This means that it is unlikely to artificially manipulate its financial numbers.

Despite Nike’s positive Beneish M score, I have concerns about its accruals. Nike’s excessive accruals indicate that its income statement may not be in line with tangible cash movements. The retail giant has seen its inventory and receivables decrease in the financial statements. This is evident when we dive deeper into their financial statements line items. The latter is not of concern, as receivables overload could be considered “masking unscollectables”. The latter is worrying as it could indicate that Nike expects a lower demand for its products in 2023.

Analyse of valuation and dividends

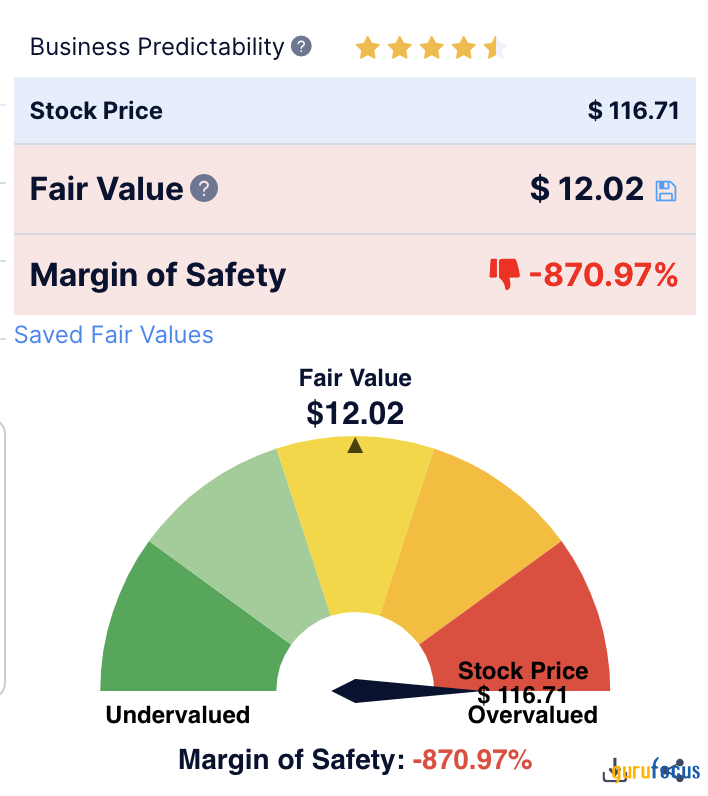

Nike’s valuation metrics are very unfavorable especially after the stock price spiked in response to the positive earnings report. A discounted cashflow model (DCF) indicates that the stock is highly overpriced in today’s marketplace. The DCF model involves discounting the future cash flows of a company (minus a discounted rate to account money’s declining value over time) in order to calculate a fair price for its stock. Below is a screenshot from my GuruFocus DCF calculation. I calculated a growth rate for the stock of 11.1% over the next ten years, and a 10% discount rate. Even with this optimistic growth projection, the stock looks overvalued.

Nike’s stock trading at 11.96x its book value indicates that ordinary shareholders hold little residual value. Nike is a mature company, and its multiples speak volumes.

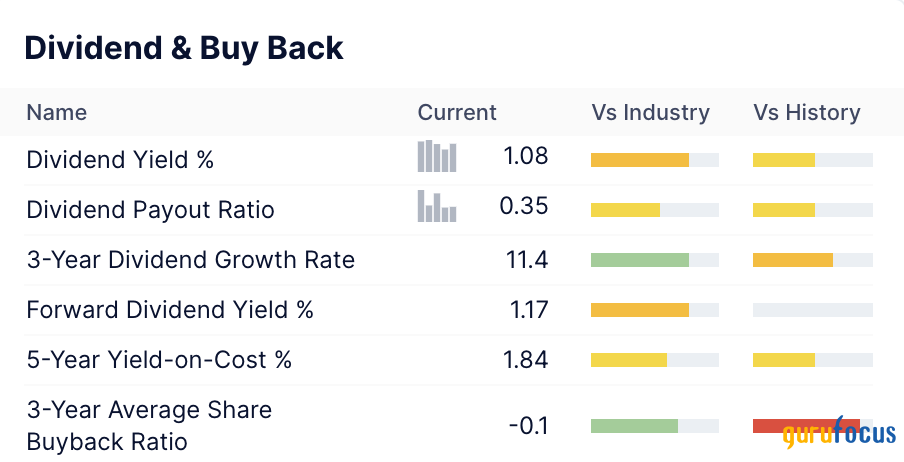

Nike stock has little value in terms dividends. The stock’s forward dividend yield A dividend coverage ratio 2.44 is associated with a dividend yield of 1.17%. Nike’s coverage ratio, although it is reasonable, doesn’t necessarily mean that the company will increase its dividend payments soon.

Technical analysis and volatility

Volatility analysis is a measure of a stock’s vulnerability to larger indices and sub-sections. In this case, Nike’s beta coefficient of 1.14x means its stock is 1.14 times as volatile as the S&P 500. Wall Street consensus is that there will be a recession in 2023. This could impact Nike stock’s prospects of being a high beta asset.

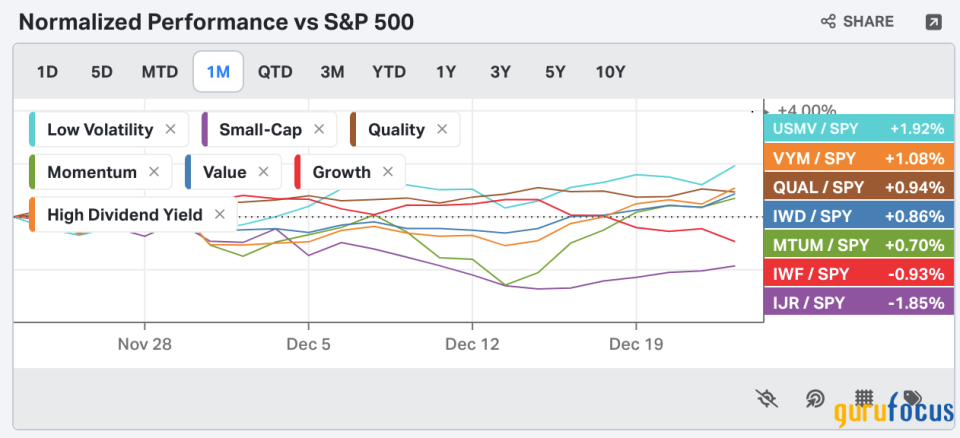

Regression analysis has shown that value, low-beta and high-dividend stocks outperformed other markets during the bear market of 2022. It is possible that the market will continue to be risk-off, and other segments could outperform in 2023.

Source: Koyfin

While there is some argument for quality, Nike doesn’t fit into any of those other segments. The beta coefficient, price multiples, dividend profile and beta coefficient are all negative. Therefore, there is no technical evidence for a Nike stock recovery in 2023.

Concluding thoughts

The company’s strong organic growth was evident in Nike’s second quarter earnings results. Many believe that Nike’s stock is too expensive since it has lost nearly 30% of its market capital value since the beginning of the year. But history shows that Nike is vulnerable to earnings crash risk which could impact its prospects. Even after the declines this year, Nike stock remains highly overvalued and doesn’t offer a very impressive dividend profile.

This article was first published on GuruFocus.