Calculating the Intrinsic Valuation Of Exxon Mobil Corporation (NYSE :XOM).

Exxon Mobil Corporation is not far (?NYSE:XOMIs it less than its intrinsic value? By using the most up-to-date financial data, we will assess whether the stock price is fair. We will take the projected future cash flows of the company. Then, we’ll discount them back to the current value. This can be achieved using the Discounted cash Flow (DCF), model. It’s not difficult, although it may seem complicated.

Our general belief is that a company’s worth is the value of the future cash it generates. But, the DCF is one of many valuation metrics, and has its flaws. You can still get answers to your burning questions about this type valuation by checking out the Simply Wall St analysis model.

See our latest analysis for Exxon Mobil

The Method

Two-stage DCF models will be used. This model, as its name suggests, considers two stages in growth. The first stage, which is usually a period of higher growth, reaches the terminal value and is captured in the second “steady growth” period. To start with, we need estimates of the next ten cash flows. If possible, we use analyst estimates. When these aren’t available, we extrapolate the previous cash flow (FCF), from the last estimate or reported amount. Companies with decreasing free cash flow will experience a slower rate of shrinkage. However, companies with increasing free cash flow should expect to see a slowing in their growth rate over the same period. This is because growth tends to slow down more in the beginning years than in later years.

A DCF is about the idea of a future dollar being less valuable than a current dollar. So we value future cash flows in relation to their value in today’s dollars.

Forecast of 10-year Free Cash Flow (FCF).

|

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

|

|

FCF Levered ($, Millions). |

US$41.8b |

US$37.7b |

US$31.9b |

US$32.7b |

US$30.8b |

US$29.7b |

US$29.1b |

US$28.9b |

US$28.9b |

US$29.1b |

|

Growth Rate Estimate Source |

Analyst x10 |

Analyst x9 |

Analyst x4 |

Analyst x2 |

Est @ -5.86% |

Est @ -3.50% |

Est @ -1.86% |

Est @ -0.71% |

Est @ 0.10% |

Est @ 0.66% |

|

Current Value ($, Millions), Discounted @ 8.9% |

US$38.4k |

US$31.8k |

US$24.6k |

US$23.2k |

US$20.0k |

US$17.8k |

US$16.0k |

US$14.6k |

US$13.4k |

US$12.4k |

(“Est”) = FCF growth rate calculated by Simply Wall St

Current Value of 10-year Cash Flow (PVCF). = US$212b

The Terminal Value is what accounts for all future cash flows in the ten year period. We use a conservative growth rate, which cannot exceed the country’s GDP. We used the 10-year average government bond yield of 2.0% to forecast future growth. As with the 10-year “growth” period, future cash flows are also discounted to today’s value using an 8.9% cost of equity.

Terminal Value (TV).= FCF2032 × (1 + g) ÷ (r – g) = US$29b× (1 + 2.0%) ÷ (8.9%– 2.0%) = US$427b

Present Value of Terminal Valu (PVTV).= TV / (1 + R)10= US$427b÷ ( 1 + 8.9%)10= US$182b

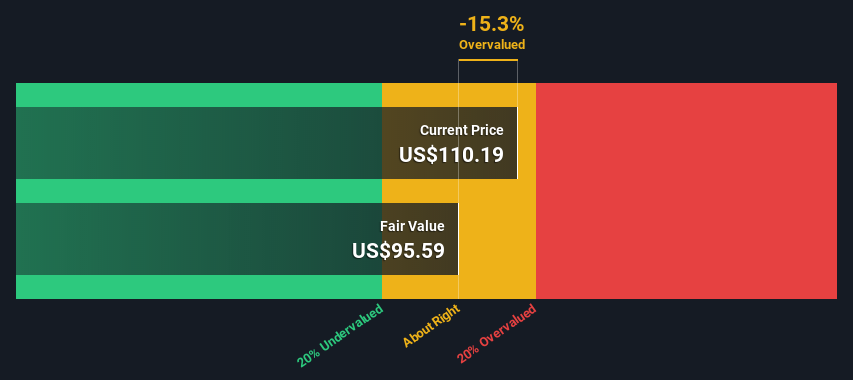

The sum of the future cash flow value and the current value of the equity is called the total value. This is US$394b. We divide the current share count by the intrinsic value to calculate the per-share share. At the time of writing, the company is fair value compared to its current share price at US$110. As assumptions can have a significant impact on valuation, it is best to see this as an estimate and not exact down to the cent.

The Assumptions

We’d like to point out that the main inputs to a discounted flow of cash are the discount rate, and of course the actual cashflows. These inputs are not mandatory. I suggest that you do the calculations again and have fun with them. The DCF doesn’t take into consideration the possible cyclicality in an industry or future capital needs of a company, so it is not a comprehensive picture of a company’s potential performances. Exxon Mobil being potential shareholders, we will use the cost to equity as our discount rate. The cost of capital (or Weighted Average Cost of Capital, WACC) accounts for debt. The calculation was based on a leveraged beta of 1.249. Beta measures a stock’s volatility in relation to the overall market. Our beta is determined from the industry’s average beta of globally comparable businesses. There is an imposed limit between 0.8% and 2.0. This is a reasonable range to consider stable businesses.

Exxon Mobil SWOT Analysis

Strength

Weakness

Opportunity

Threat

Looking ahead:

While the DCF calculation is important, it shouldn’t be the only piece of analysis that you examine for a company. DCF models aren’t the only tool for investment valuation. You would prefer to use different assumptions and cases in order to determine how they impact the company’s value. The output of a company can be very different if it grows at a different pace or its cost of equity changes rapidly. Three additional elements are available for Exxon Mobil. We recommend further investigation.

-

There are risks: This is a good example of what we have spotted. 2 warning signs for Exxon Mobil There are a few things you need to be aware of.

-

Future EarningsXOM’s growth rate compared to other companies and the larger market Our interactive web site allows you to dig deeper into the analyst consensus numbers for the coming years. free analyst growth expectation chart.

-

Other solid businessesTo be a successful business, you need to have low debt, high returns on equity, and strong past performance. Look around! our interactive list of stocks with solid business fundamentals To find out if there are any other companies that you might have not considered.

PS. PS. You can also find the calculations for other stocks here search here.

Give feedback about this article Are you concerned about the content? Get in touch Contact us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St has a general nature. We only provide commentary on historical data and analyst projections. Our articles are not meant to be considered financial advice. It is not a recommendation not to buy or sell any stocks and does not take into account your financial situation or objectives. We strive to deliver long-term focused analysis that is based on fundamental data. Our analysis may not take into account the most recent price-sensitive company announcements and qualitative material. Simply Wall St holds no position in any of the stocks mentioned.

Register for a paid user research session

You’ll receive a Amazon Gift Card: US$30 Spend an hour helping us to create better tools for individual investors. Sign up here