Here are 5 Reasons You Should Keep Inari Medical (NARI), Stock Now

Inari Medical, Inc. NARI has a strong foundation for growth. This is due to its dedication to understanding the vein system and the huge market potential for products. But, dependence on broad acceptance of products is a concern.

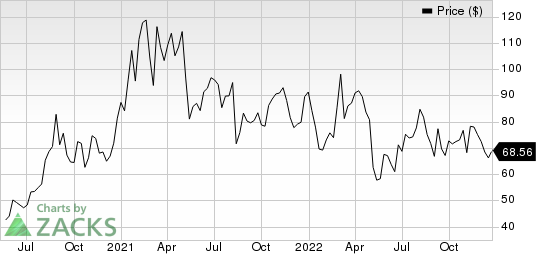

Shares of this Zacks Rank #3 (Hold) stock have lost 25% compared with the industry’s decline of 27.9% on a year-to-date basis. The S&P 500 Index has fallen 20% in the same time frame.

NARI — with a market capitalization of $3.67 billion — is a commercial-stage medical device company that seeks to develop products to treat and change the lives of patients suffering from venous diseases. The company’s earnings yield of (0.9%) compares favorably with the industry’s (9.2%). It beat the earnings estimates in three quarters, and it matched them in one quarter. The average surprise was 15.81%.

Image Source: Zacks Investment Research

What’s Driving Its Performance?

Inari Medical is responsible for the creation and marketing of purposely built devices, taking into consideration the specific characteristics and diseases of the venous system and the unique clot pattern. The company’s commitment to understanding the venous system and in-depth knowledge of its target market has allowed it to figure out the unmet needs of its patients and physicians. NARI’s ability to innovate quickly and improve its products has allowed it to inform its educational and clinical programs.

Inari Medical reported positive in-hospital and 30-day outcomes data for the CLOUT deep-vein thrombosis registry. The company also reported positive results from a propensity-matched comparison of patients treated in the CLOUT registry compared to patients treated with pharmacomechanical thrombolysis in an NIH-sponsored randomized controlled trial — ATTRACT. ClotTriever patients experienced complete thrombus clearance at a rate that was nearly twice that of patients who received ATTRACT’s intervention arm. ClotTriever treated significantly fewer patients with PTS (post-thrombotic syndrome) than the ATTRACT intervention arm. The absolute drop in PTS was 13% over 30 days. ClotTriever was found to remove more clots and had better patient outcomes. It also showed lower PTS rates. This will likely lead to greater adoption by physicians and patients.

The company revealed positive results of its fully enrolled FLASH registry for pulmonary embolism (PE) earlier this year. FlowTriever, a company that treats PE, met the primary endpoint of this registry. A PEERLESS randomized controlled study is being conducted by the company in PE patients.

Inari Medical reported that many DVT and PE patients are treated using conservative medical management, which only uses anticoagulants. These drugs do not dissolve or remove existing clots. According to Inari Medical, there is a large untapped market for effective and safe treatment of existing clots in patients suffering from these conditions.

In March, the FDA granted approval to Artix. This peripheral thrombectomy device was created to address unmet medical needs in a new patient group. This is the first part of a larger toolbox that the company is currently developing. ClotTriever Bold was released to the market in a limited release last year. The company then went on to release ClotTriever Bold for full-market. Bold is a more aggressive version of the company’s original ClotTriever device.

Due to strong procedural growth across both ClotTriever & FlowTriever product line lines, revenues in the third quarter of 2022 jumped 32% over the previous-year quarter. Going forward, the positive trial data will likely increase top-line growth. During the third quarter, Inari launched two new products — Protrieve and InThrill — bringing its total new product launches this year to six. InThrill is a $1 billion market opportunity, according to Inari.

What’s Weighing on the Company?

Most of Inari Medical’s product sales and revenues come from a limited number of hospitals. The company’s growth and profitability mainly depend on its ability to boost physician and patient awareness of its products and how keen physicians and hospitals are to adopt its products and perform catheter-based thrombectomy procedures for the treatment of venous thromboembolism.

The company’s inability to show the benefits of its products and catheter-based thrombectomy procedures will result in limited adoption of the same. It may not occur as quickly as anticipated, which could negatively impact its business and financial situation.

Inari Medical, Inc. Price

Inari Medical, Inc. price | Inari Medical, Inc. Quote

Estimates Trend

For 2022, the Zacks Consensus Estimate for revenues is pegged at $374.7 million, indicating an improvement of 35.3% from the year-ago period’s reported figure. The revenue is expected to rise by nearly 20% in 2023. For the bottom line, it is expected to lose 61c per share by 2022. It reported adjusted earnings per share of 18 cents for the year-ago period. Earnings estimates indicate a 62.3% improvement in 2023.

Stocks to Take into Account

These stocks are among the best-ranked in the wider medical space. Elevance Health ELV, Merit Medical Systems MMSI HealthEquity HQY has a Zacks Rank number 2 (Buy). You can view the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Elevance Health’s earnings per share has risen from $28.97 to $29.02 for 2022 and from $32.58 to $32.63 for 2023 in the past 60 days. ELV has risen 10.2% this year. Elevance Health’s earnings surprise was 4.11% in the four most recent quarters.

Merit Medical Systems’ earnings have increased from $2.47- $2.57 for 2022, and $2.77- $2.82 in 2023 over the past 60 days. MMSI stock has increased 13.1% this year. Merit Medical Systems has delivered an average earnings surprise of 25.35% over the past four quarters.

Estimates for HealthEquity’s earnings per share have increased from $1.28 to $1.29 for fiscal 2023 and from $1.76 to $1.79 for fiscal 2024 in the past 60 days. HQY has risen 39.6% this year. HealthEquity’s earnings are anticipated to improve 26.3% over the next five years.

Want the latest Zacks Investment Research recommendations? Download 7 Best Stocks in the Next 30 Days Today Click to get this free report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report

Inari Medical, Inc. (NARI) : Free Stock Analysis Report

Elevance Health, Inc. (ELV) : Free Stock Analysis Report